Will Getting Pre-Approved Hurt Your Credit?

If you’re thinking about buying a home, you probably know that your credit plays an important role in getting approved for a mortgage. The better your credit score, the better your terms usually are, so making sure you have the best score possible is important.

However, you’ve likely also heard that getting pre-approved can hurt your credit score. You also know that you need to get pre-approved (unless you are paying cash) because that will tell you what houses you can shop for.

So if you’re supposed to get pre-approved, and the lender needs to check your credit what should you do?

Understanding Your Credit Score

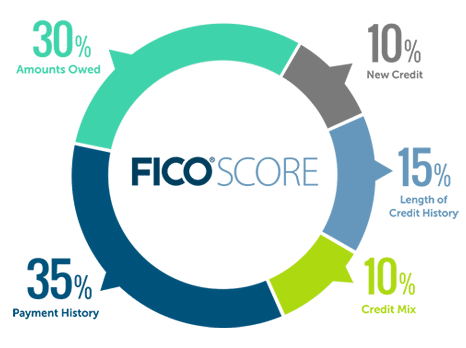

Your credit score is made up of five different factors, and understanding them will help you know what to do next.

The 5 Factors that affect your Credit Score:

- Payment History 35%

- Amounts Owed 30%

- Length of Credit History 15%

- Credit Mix 10%

- New Credit 10%

These five factors are how the credit bureaus determine your FICO scores, and as you can see how much you borrow and how well you repay your debts are the two most important categories.

The category that most deals with mortgage pre-approvals are your Credit Mix. Credit Mix is 10% of how your credit score is factored. When a lender or bank pulls your credit this is known as a credit inquiry. Having too many credit inquiries in a short period of time can negatively affect your credit score.

How to How to Fix Your Credit to Buy a HomeFix Your Credit to Buy a Home

There are two types of credit inquiries you need to know about:

Hard Inquiries

Hard credit inquiries are inquiries that will show up on your credit report, and these typically occur when you apply for a loan or credit card.

Examples of Hard Inquiries:

- Shopping for a Car and Applying for Financing

- Applying for a New Credit Card

- Requesting Credit Line Increases on Your Credit Card

- Mortgage Pre-Approval

Soft Inquiries

Soft inquiries are inquiries that are made on your credit, but they do not show up on your credit report, and therefore do not affect your score.

Common Soft Inquiries Include:

- Checking your credit yourself

- Your bank seeks an update on your credit report

- Credit card companies sending you pre-qualified offers

Will Credit Inquiries Affect Your Credit Score?

According to Myfico.com the company that creates your fico score,

“The impact from applying for credit will vary from person to person based on their unique credit histories. In general, credit inquiries have a small impact on your FICO Scores. For most people, one additional credit inquiry will take less than five points off their FICO Scores.”

So as you can see it’s certainly possible that credit inquiries can lower your score, the effect they have is generally very small versus other factors. Also, the rules for rate shopping are different than those for applying for new lines of credit.

Again according to Myfico.com

“ Looking for new credit can equate with higher risk, but most Credit Scores are not affected by multiple inquiries from auto, mortgage, or student loan lenders within a short period of time. Typically, these are treated as a single inquiry and will have little impact on your credit scores.”

How Long Will Inquiries Remain on Your Credit Report?

Hard inquiries will show up on your credit report for 2 years from the date that your credit was pulled. However, the credit bureaus will only factor them into your credit score for 12 months from the date your credit report was pulled.

How Does a Mortgage Pre-Approval Affect Your Credit Score?

So how does a mortgage pre-approval affect your credit score, the answer is very little. Getting pre-approved wont hurt your credit score. You might see at most a 5 points drop from the first lender who pulls your credit, but no noticeable effect after.

This is because the credit bureau will treat all subsequent credit inquiries related to getting a mortgage the same.

Another plus is that when you work with a mortgage broker, like Bayou Mortgage, we can pull your credit one time and shop hundreds of lenders for you in about five minutes.

Also, soft credit pulls are becoming common in the mortgage industry, especially as a way of getting a pre-approval. If you are using one of the big online lenders, chances are they are only going to do a soft credit pull until you go under contract, but this can be problematic as we’ll discuss below.

What is a Mortgage Pre-Approval?

A Mortgage Pre-Approvalis a process that homebuyers go through when they are ready to start shopping for a home. In order to get a pre-approval, you need to complete a mortgage application and provide supporting documentation.

Steps of the Pre-Approval Process:

- Speak with a Loan Officer

- Complete Mortgage Application

- Allow Lender to Pull Your Credit Report

- Provide Documents

- Start Shopping for a Home

Providing a complete mortgage application with all the necessary documents is the only way to have a true pre-approval. While many online lenders are doing soft credit checks and doing short mortgage applications, these are not real pre-approvals.

If you haven’t provided authorized a tri-merged credit report, provide documents that support your income and assets you are asking for a disaster.

Why You Should Get Pre-Approved

Getting pre-approved is important because you can’t confidently look for homes without one. If you don’t have a pre-approval letter, many realtors won’t show you homes. Even if they do show you homes, you have no real idea if you will be approved to purchase the home.

A pre-approval eliminates the doubt and anxiety that comes with buying a home. When you work with a reputable loan officer, a pre-approval will allow you to shop with the same confidence as a cash buyer.

Bottom Line

Getting pre-approved will provide you with peace of mind, and make your home buying experience a lot smoother. Working with a lender and doing the hard work upfront will ensure that you know what to expect upfront, and will eliminate costly mistakes later.