What’s Included In My Mortgage Payment?

So you’re thinking about buying a home but you want

9 Reasons to Choose a Mortgage Broker

1. Get independent advice on your financial options. As independent

USDA Rural Development Loan: The Complete Guide

Buying a home when you don’t have money for a

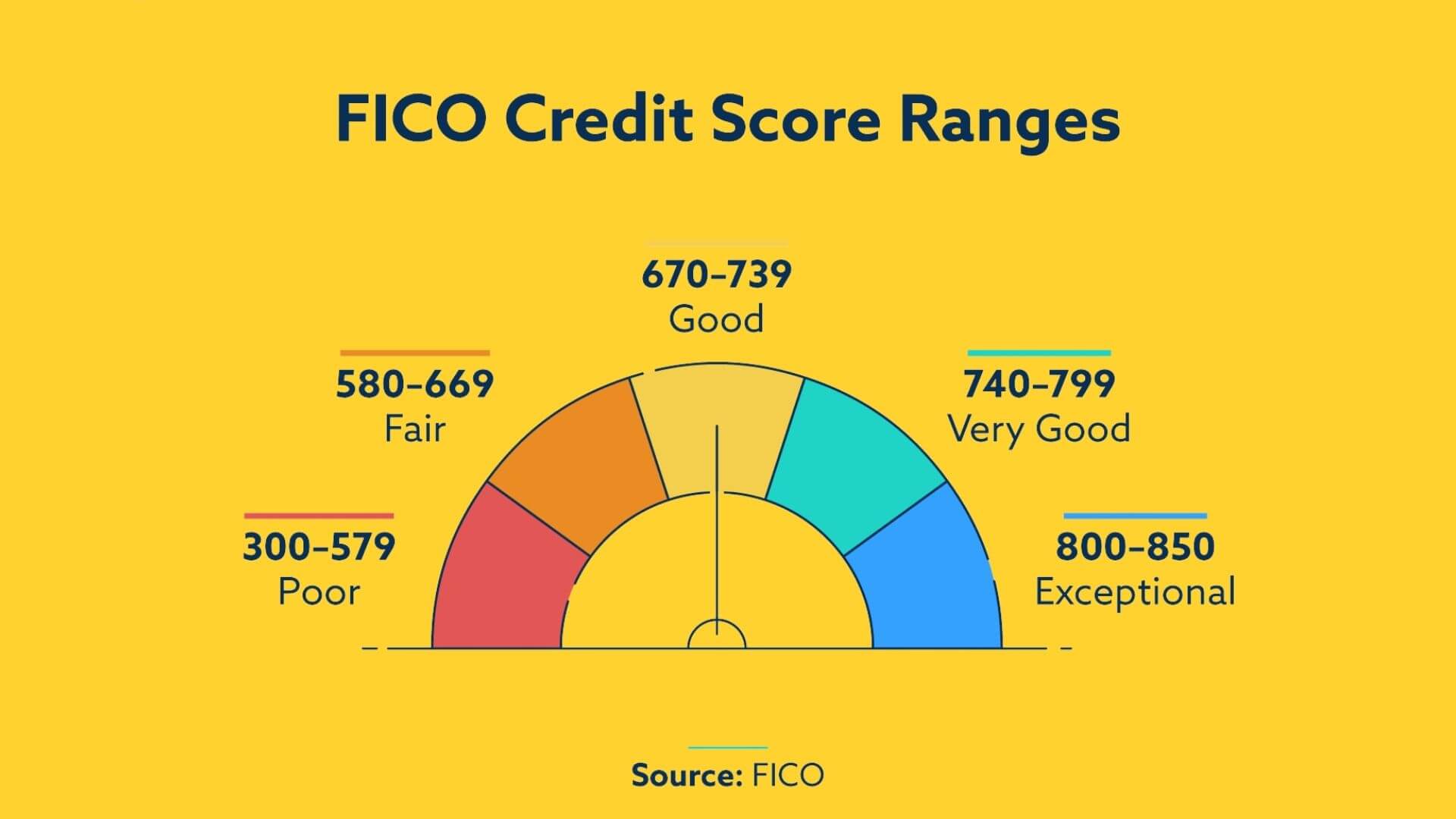

The Complete Guide to FHA Loans

FHA loans are great for borrowers with less than perfect

Refinancing Your Mortgage- The Complete Guide

Are you considering refinancing your home? Maybe you want to

How To Buy a Home With Your Tax Refund

Are you renting or still living with your family? Do