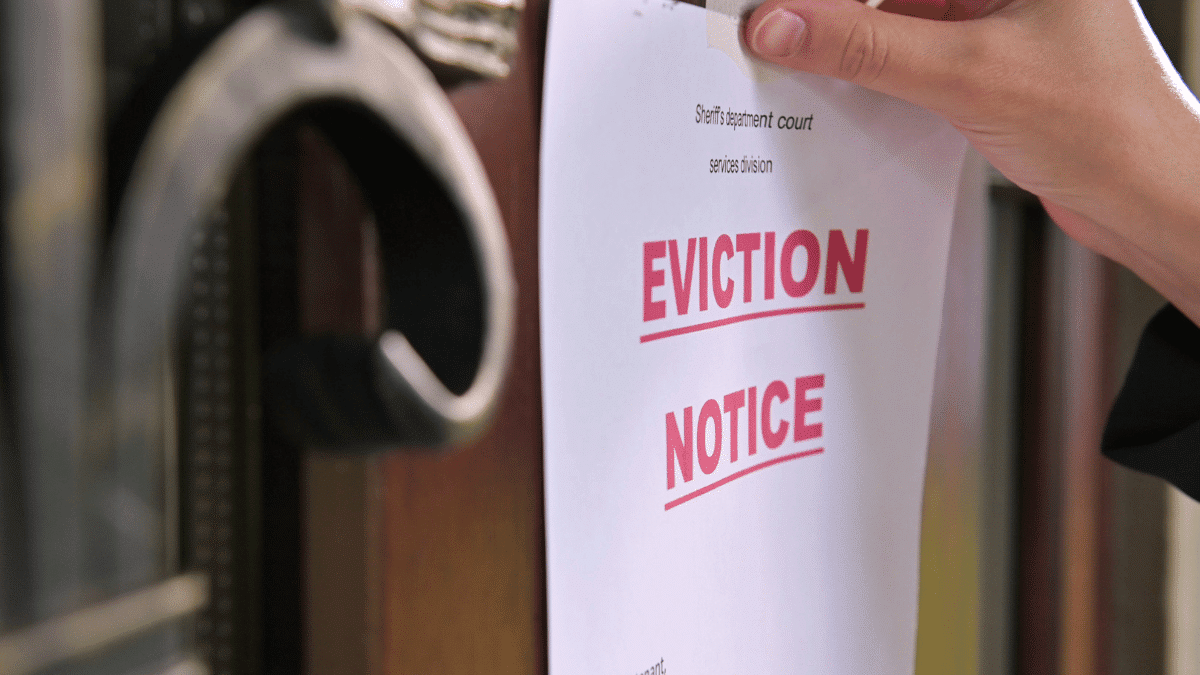

Does an Eviction Affect Your Ability to Buy a House?

Does an Eviction Affect Your Ability to Buy a House?

What Is A Conventional Loan?

Understanding Conventional Loans A conventional loan is much like the

HELOC vs. Cash Out Refinance

When looking into HELOC vs. cash-out refinance, homeowners have two

HELOC vs. Home Equity Loan

What’s The Difference Between HELOCS And Home Equity Loans? A

Second Mortgage: What They Are and How They Work

Everyone has heard the term second mortgage, but what does

What is a 15 Year Fixed Mortgage?

What Is A 15-Year Fixed Mortgage? A 15-year fixed mortgage

What is a 30 Year Fixed Rate Mortgage

What Is A 30-Year Fixed Mortgage? A 30-year fixed mortgage