What is a 30 Year Fixed Rate Mortgage

What Is A 30-Year Fixed Mortgage? A 30-year fixed mortgage

What is a 15 Year Fixed Mortgage?

What Is A 15-Year Fixed Mortgage? A 15-year fixed mortgage

Second Mortgage: What They Are and How They Work

Everyone has heard the term second mortgage, but what does

HELOC vs. Home Equity Loan

What’s The Difference Between HELOCS And Home Equity Loans? A

HELOC vs. Cash Out Refinance

When looking into HELOC vs. cash-out refinance, homeowners have two

What Is A Conventional Loan?

Understanding Conventional Loans A conventional loan is much like the

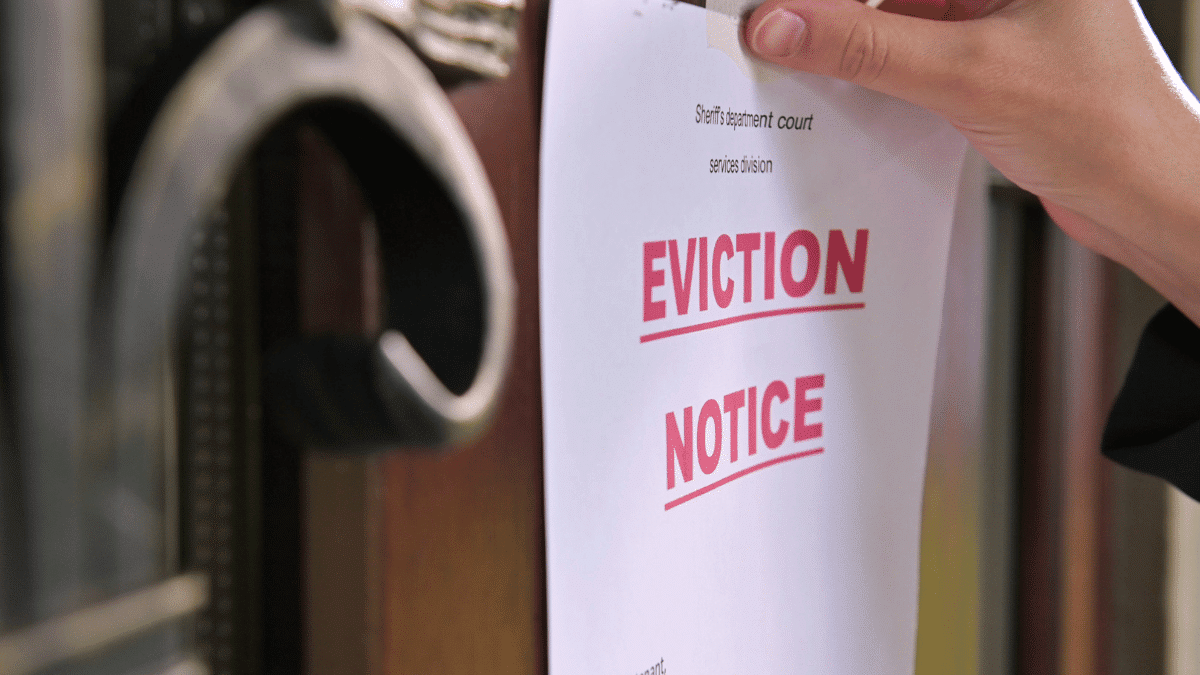

Does an Eviction Affect Your Ability to Buy a House?

Does an Eviction Affect Your Ability to Buy a House?