The housing market is going to crash! Or is it?

It seems like it wasn’t that long ago that every home listed on the market would sell in a matter of hours or days at most. Sellers were getting over the list price for their homes and buyers were having to make offers on 10+ homes just to win one.

Will this trend continue now that we are seeing record-breaking inflation and interest rate increases? While no one has a crystal ball…the question now is will the housing market crash?

With the cost of everything rising is the economy in bad enough shape to crash the housing market? Let’s take a look!

Is the housing market going to crash?

The last time we were this concerned about the housing market (and the economy in general) was 2008. During those years, the United States and the world saw a deep and dark recession that lasted several years. This recession was the worst since the Great Depression.

A combination of rapid home appreciation, loose mortgage lending criteria, and an insatiable appetite from Wall Street led to the biggest housing bubble and subsequent crash we’ve ever seen.

So are we looking at a similar housing crash now? Not according to Moody’s chief economist Mark Zandi:

“We’ve officially moved from a housing boom into a housing correction,” He continues, “ The lack of mortgage defaults and distressed sales will keep housing prices from falling too much. That’s when you get crashes – when you have lots of foreclosures and a lot of distressed sales.

“That’s just not going to happen”

So will the housing market shift?

I believe the housing market is going to shift and we are already seeing the beginnings of this process. There are simply too many factors at hand to keep this rapid appreciation going.

Factors that Contribute to a Housing Market Shift

There a few factors that we are currently seeing that signal a housing market shift over the next 12 months. Let’s take a look at them.

Rapidly Rising Interest Rates

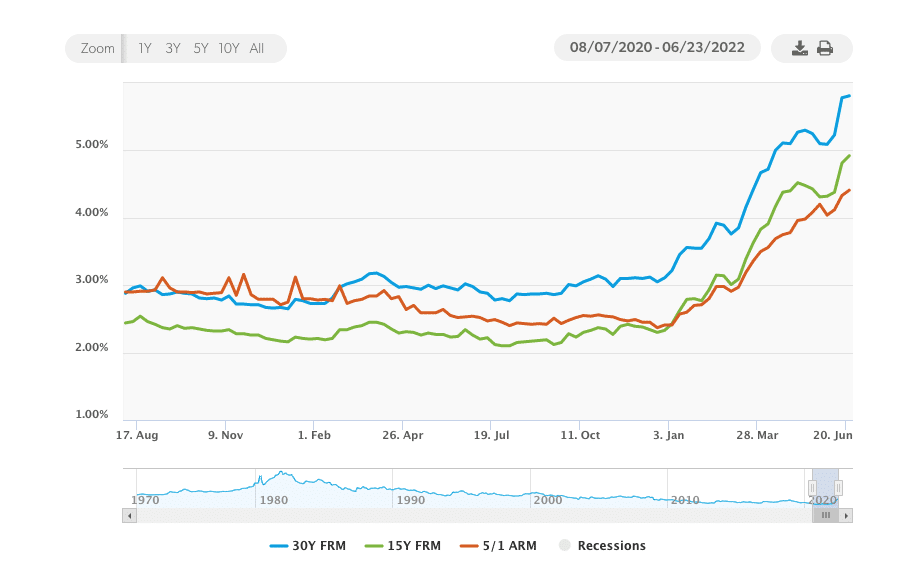

The biggest factor that’s currently causing the market to slow down is the rise in interest rates. In the last two years, we have experienced record-breaking mortgage rates on both ends.

First, we saw the lowest mortgage rates ever recorded in history. Much of this was fueled by the COVID-19 pandemic and record-breaking purchases of Mortgage-Backed Securities by the Federal Government.

Now in 2022, we’ve seen the largest spike in interest rates since 1987. As you can see in the chart below, rates have risen nearly 3% in the first 6 months of 2022.

However, it’s also extremely important to remember that the mortgage rates we are seeing now, are fairly normal. In fact, we saw interest rates in 2016 that were around 5%, and historically speaking rates throughout the years have averaged much higher than where we are now.

Rising Inflation

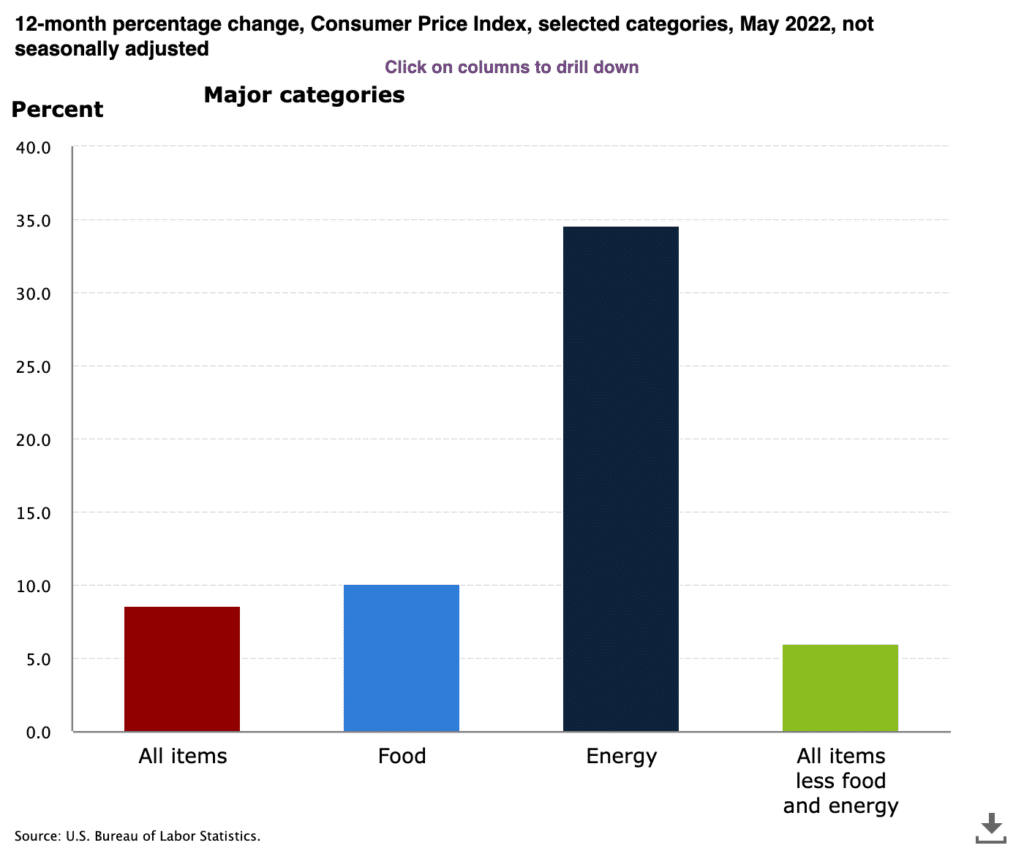

Another impact to the housing market shift is rising inflation. The latest inflation reports from May tell us that inflation has risen 8.3% YTD.

This doesn’t tell the whole story though…

Most of the consumer products and necessities we buy have risen much higher than this. Gas prices, food, electricity, home goods, etc., have all increased much higher than this and are no doubt putting a strain on families across the country.

Less cash means fewer people buying things, including homes, and we are already starting to see that data come in.

Mortgage Applications

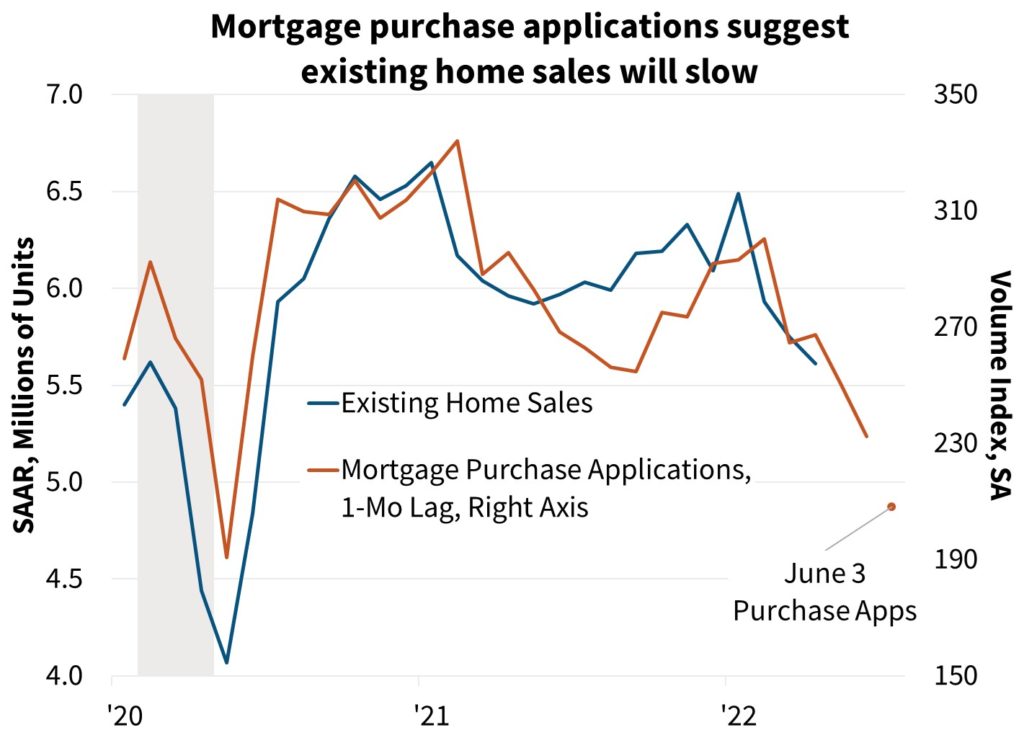

Recent data from Fannie Mae shows mortgage applications sharply falling as you can see in this graph. Mortgage applications can be a precursor to lower home sales which are also beginning to decline.

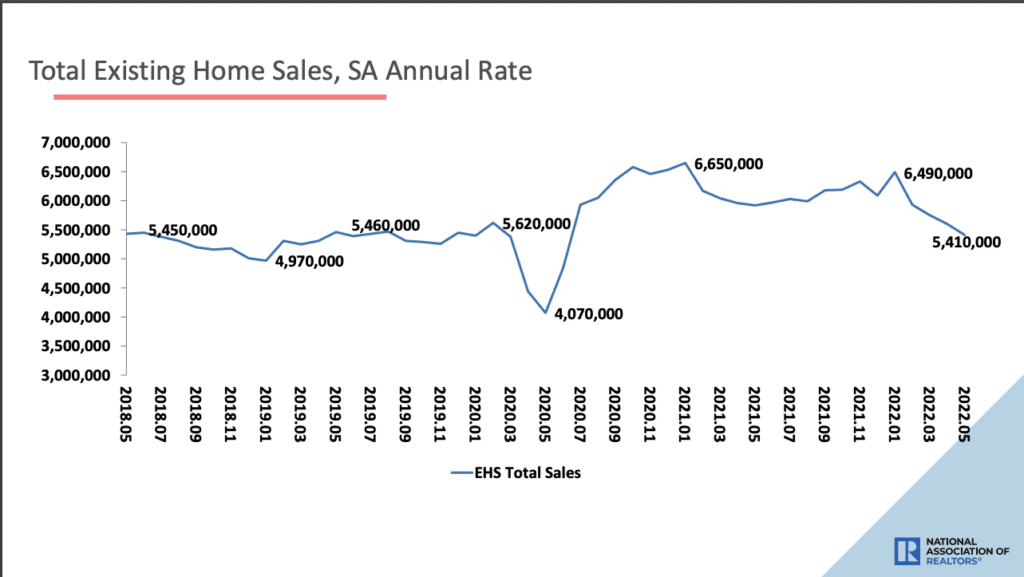

Existing-Home Sales

As you can see, existing home sales fell 3.4% in May – which is the fourth consecutive month it has declined. YTD existing home sales are down 6%.

We are also seeing that the number of homes available on the market increased by 12.6%, moving up the months of supply to 2.6. This is its highest level since August of 2021.

The only outlier in the data is that recent home sales have increased 10.7%, but still, YTD new homes sales are down 10.6%

Slowing home sales and inventory on the market go hand in hand. As purchases slow down, we’ll see more inventory. More inventory will make it easier for potential buyers to get their offers accepted.

So will the housing market crash in 2022?

It’s not likely…

While we are obviously beginning to see a slowdown in home sales and an increase in available inventory, this is more of an adjustment. We are coming down from record highs in home sales and appreciation. This is likely to be more of a leveling out than a crash.

Real Estate is Local

It’s important to remember that real estate is local. There are some really hot real estate markets in cities like Phoenix, Boise, Northwest Florida, and others. In these areas where home prices are very inflated, there is more risk of a bubble.

For most other areas, the risk is low.

Is the housing market going to slow down?

Yes, it will. In fact, as we’ve already discussed it’s happening now. This is good news for buyers who are looking to purchase a home.

This will give you an opportunity to find a house more easily and have less competition when you do make an offer.

Read:The Housing Market Is Slowing Down- Here’s Why

How much the housing market slows down will depend on a few different factors:

- Inflation

- Mortgage Rates

- Inventory

- Unemployment

If we continue to see rising interest rates and rising inflation, but inventory remains low, the slow down will be, well, slow.

However, if we enter into a period of stagflation where unemployment increases, and inflation keeps rising or stays the same, that could change.

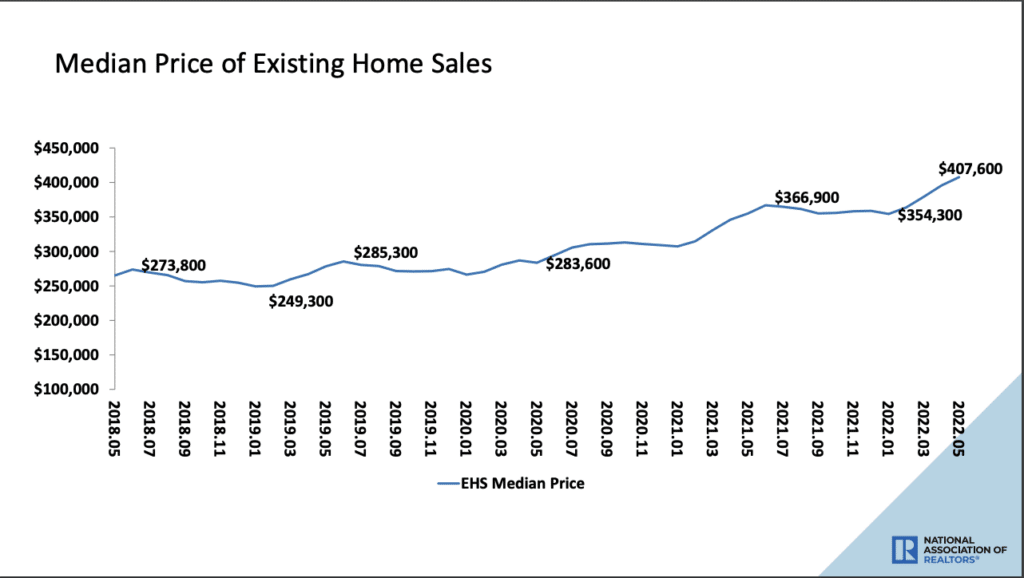

Are Home Prices Dropping?

It’s not likely in 2022.

The reason home prices aren’t expected to drop is due to inventory. In most markets across the country, inventory remains low.

Supply and demand is at play here. Until demand lowers significantly or supply increases significantly, the prices are here to stay. While prices aren’t expected to drop, I do think we are seeing the breaks get pumped on runaway appreciation.

5 Reasons The Housing Market Isn’t Crashing Soon

1. Inventory Remains Extremely Low

There is simply not enough inventory right now to balance out the current demand in the housing market. A housing crash happens when home prices bottom out and demand dries up. There is still too much demand for this to happen.

While higher interest rates and rising inflation will cause the housing market to correct and slow down, most places simply still don’t have enough inventory to meet demand.

2. We’ve been Under built Since 2007

During the last housing crisis, builders skyrocketed the construction of new homes to meet the demand of the market. The problem was that the market was artificial, people were buying homes and speculating because of the rapid increase in home values.

Most of this was due to the loose requirements and market demand for more MBS (mortgage-backed securities).

We just came out of an extreme supply crunch with the pandemic which saw the cost of materials rapidly increase. There is also more red tape when it comes to being able to buy up land and build.

While most of the builders are ramping up production as the cost of lumber drops, the overbuilding we saw from 2005 to 2007 is unlikely.

3. Lending Standards Are Much More Strict

In order to meet the demands of the market and wall street, most lenders drastically reduced their lending standards so more people would qualify.

You had “liar loans”, which were loan programs that only required a signed mortgage application in order to be approved.

You did not have to prove your income or employment, or provide a down payment. This resulted in people purchasing homes they could not afford with no equity.

As we sit today, mortgages aren’t as easy to get. The requirements to get a mortgage are tougher, and everything must be backed up with substantial documentation.

4. Foreclosure Risk Remains Low

We don’t have nearly the foreclosure risk we did in 2007. Americans are in much better shape today than they were then. We have more equity in our homes, more cash in the bank, and much lower unemployment.

While we certainly need to keep an eye on these things as we progress through this next recession, we have a long way to go to reach the levels of the last recession.

5. Unemployment Remains Low

As mentioned above unemployment remains low. In fact, many businesses are still finding it difficult to find workers as we open back up from the pandemic.

The supply issues we have in the real estate market are some of the same issues in other industries.

As long as demand continues to outpace supply, most companies should remain in good shape. As inflation goes on, we will see demand come down, but it should not rise to a level that will cause massive layoffs across multiple industries.

Housing Market Prediction for 2022 and beyond

The housing market is certainly shifting and this has many fearful. I think a lot of the fear is understandable given our most recent memory of a housing market contracting.

This is not 2008. Not even close.

For the remainder of 2022, you will continue to see slowing home sales as the market digests the rising rates and inflation we are experiencing.

According to Selma Hepp, deputy chief economist for CoreLogic:

“The market will continue to see relatively strong demand from buyers and an elevated rate of home price growth, despite slowing notably from ultra-hot early spring 2022 conditions”

While home sales will continue to decline and available inventory should begin to slowly increase, I would not count on prices coming down. There is still an inventory issue and that isn’t going to go away overnight.

As long as inventory remains low, the price of homes will continue to appreciate, even if it is slower.

Prediction for 2023 and Beyond

As we enter into 2023, Fannie Mae thinks home prices will decline sharply.

However, it’s important to keep in mind that much of the price appreciation we’ve seen over the last two years is artificial.

The COVID-19 pandemic created huge issues for the production of supplies. Double-digit home price appreciation is not the norm.

Much of what happens in the next 5 years is going to depend on how deep the recession goes. While we are experiencing rising inflation, there are fears that we could begin to experience stagflation which will further depress the economy.

If we can curb inflation, keep wage growth high, and avoid massive unemployment, the housing market will be more of a return to normal.

Should I Buy a House Now or Wait?

So is now the right time to buy a house? Should you wait to buy a house?

Fair questions…

I think it depends on your current situation. Buying a house like anything else ,is about you. The interest rates are higher than they were a year ago but they aren’t much higher than what’s normal, even before the pandemic.

Home prices have rapidly increased in some areas but not everywhere. Here are a few questions you should ask yourself to see if you should buy a house.

1. Do you have a budget?

The biggest mistake I see homebuyers make is not having a robust budget. You need to know what you are spending every month. I am not just talking about your big bills. Pull out those bank statements and see exactly where every dollar you spent went.

When budgeting we often forget about:

- Subscriptions (Like Netflix or Spotify)

- Restaurant and Fast Food

- Entertainment

- Personal Care

- Pet Care

These are just a few categories, you should have a zero-based budget so you know where every dollar is going. Only once you know where your money is going can you understand what you can spend each month on your mortgage payment.

2.Have you saved for a down payment or closing costs?

You are going to want to make sure you have prepared for the out-of-pocket expenses that come with getting a house. There are no down payment programs and options to have your closing costs paid, but you’ll be more competitive if you can pay them yourself instead of asking a seller to pay them for you.

In addition to your standard down payment, it’s not a bad idea to have some type of emergency fund.

3.How long will you stay in the home?

If you want to purchase a house you need to think about how long you plan to stay in the home. If you are going to stay in the home long term, then right now should be a good time to buy. Fluctuations in your home’s value will affect you less over time and interest rates are expected to fall once we curb inflation. The longer you stay in the home the less a potential housing market crash will affect you.

This means you’ll have the opportunity to refinance your mortgage to the lower rate when rates do fall. Don’t miss out on the opportunity to start building equity in your home now, hoping that prices or rates will fall soon… because that’s not likely.

Reasons You Should Wait to Buy a House

1.Your credit or finances aren’t in order

The most expensive way to purchase a house is with poor credit. The rate you will pay will be much higher if you have a low credit score. It’s not as difficult as you may think to fix or repair your credit.

Check Out How to Fix Your Credit To Buy a House

If you have concerns about your credit, your savings, or your employment it’s probably best to wait until you get those things fixed. However, there are times were moving is urgent and using a program that allows bad credit can be helpful.

2. You won’t be in the home long

If you want to purchase a house, but you know that you’ll need to move in the next 5 years, it’s probably best to rent or wait. It could be more difficult for you to sell the house or break even on the cost of acquiring it if you are going to be moving in the next 5 years.

The Great Housing Market Crash of 2022… Isn’t Going to Happen

I know many of you would love to be able to purchase a house for $50k with a 3% interest rate as your parents or grandparents did, but I don’t think that’s happening anytime soon.

Buying a house is like planting a tree, the best time to buy was 30 years ago but the next best time to buy is today. If you want to own a house and you are currently paying rent, don’t let the news scare you.

Avoid buying a house that’s more than you can afford, plan to hold on to it for a while, and you’ll be fine.