You probably know that when you are buying a home there are certain costs involved. You know that you likely need a down payment and that there will be some fees along the way. What many first-time homebuyers don’t consider is mortgage closing costs. Knowing what these closing costs in Louisiana are and how much to set aside will help to ensure you aren’t caught off guard ( and you might not need to pay them!)

What are mortgage closing costs?

Closing costs are fees that are charged to you the buyer by all of the parties involved in the home buying transaction. While the seller has closing costs of their own, most of the costs fall on the buyer in a mortgage transaction. These are fees for work performed by each person who helps you get to the closing table.

What are the average closing costs in Louisiana?

While it’s important to note that these costs due vary from place to place and person to person, there are some average costs you can expect.

Average Louisiana closing costs for home buyers will typically run from 2%-5% of the total purchase price of the home. More expensive homes will fall in the 2% end and less expensive homes would be closer to 5% If you are purchasing a home for $300,000 your costs would likely fall between 2-3% of the cost of the home. A $100,000 home would be closer to 5% of the cost of the home.

Other factors that can increase your cost of buying a home:

- Low credit scores

- Low down payment

- Homes in a flood zone

- Older homes

- Homes or clients that have a higher insurance risk

RELATED 👉 5 Ways To Save For A Down Payment

Who Can Pay For Louisiana Closing Costs?

The closing costs are the responsibility of you the buyer. However, if you are a savvy negotiator you can request the seller to cover some or all of your closing costs. FHA and USDA allow the seller to cover up to 6% of the purchase price in what’s known as seller concessions.

Conventional Loans range from 3%-6% depending on your down payment. If you put less than 10% down the seller can cover 3% of your costs. If you put more than 10% down the seller can cover up to 6% of your costs. VA loans would allow the seller to cover up to 4% of the purchase price in seller concessions.

RELATED 👉 Moving to Louisiana?

Costs Associated with the Home

When going through theprocess of buying a home you will have two to three out-of-pocket costs that you have to pay for upfront.

💵 Earnest Money or Deposit

When making an offer on a home many sellers will require you to put money up as a deposit once you go under contract. This is to make sure that you have skin in the game and to protect the seller.

The cost of your earnest money deposit can vary from $1,000 to 1% of the purchase price of the home. This is typically a matter of negotiation between the buyer and the seller.

The good news is that any money put toward a deposit will be credited to your closing costs and down payment ( if it’s your own money)

🧑🔧 Home Inspection Fees

The home inspection is not required by your lender but it is highly recommended to help you discover any defects in the property. The home inspection is generally completed during the inspection period of buying a home. This is a time when you can typically walk away from the home without cost or penalty but again consult with your agent.

The price of a home inspection may vary but generally, the cost is between $300- $500 depending on the size of the home and scope of the work.

👉 Read: How Much is a Home Inspection In Louisiana?

🏡 Home Appraisal Costs

A home appraisal is an important step in being approved for a loan when buying a home. The home appraisal tells you and the lender what the home is worth. The appraisal is performed by a licensed appraiser in your area and the report is returned to the lender.

You cannot shop for an appraiser on your own due to mortgage regulations. The lender will order the appraisal from an appraisal management company who then selects bids for the job. The average cost of an appraisal in Louisiana is between $500-$600. In other places around the country with higher purchase prices the cost can be 2-3 times that amount.

You should be prepared for these three charges when buying a home. They will most often be required upfront and the service will not be provided until payment has been received.

Only the home inspection is not deducted from your overall closing costs. The appraisal and escrow money are credit back to you and deducted from your overall costs due at closing.

👉 Read: LOUISIANA FIRST-TIME HOMEBUYER GUIDE

Mortgage-Related Fees

Application Fee

Some lenders may choose to charge their clients an application fee in order to work with them. This would be an upfront charge from the lender to begin the process of working with them.

At Bayou Mortgage we do not charge any application fees to our clients to start working with us. We have heard that many of our online competitors charge application fees as much as $500! Our advice would be to steer clear of any company demanding you pay an application fee to work with them.

Loan Origination Fees

These are the fees charged by your lender in order to originate your loan. They take many different names but all boil down to the same thing. Some lenders may call them an underwriting fee, admin fee or processing fee, or any combination of them.

This is one of two fees where you want to shop to find the best deal. Many times a lender can have a lower rate or a similar rate to another lender, but their loan fees will be much higher.

Interest rate and loan fees go hand in hand so you will definitely want to take the time to find the best overall deal. (Or just shop with a mortgage broker and they can handle that for you)

Costs Examples for Loan Fees

- Underwriting or Admin Fee: $800-$1500

- Processing Fee $500-$900

The average loan has about$1500 in lender or loan fees but this is something that can be negotiated so ask!

Discount Points

A point is simply a percentage of the loan amount. So 1 “point” is equal to 1%. If you were buying a $200,000 home, then 1 point would be $2000.

Typically you will pay discount points to lower your interest rate. If you’ve ever wondered how low your interest rate can be the answer is simple: As low as you want! With enough cash, you can buy down your rate to where you want it.

The better question is, should you? You may be surprised to find that a lower interest rate can costs you thousands of dollars upfront while making less than $100 difference per month.

The other scenario where discount points can come into play is with lower credit score buyers. If you have less than perfect credit (under 620) you could be required to pay discount points in order to get the loan.

This is usually a result of the risk your credit profile presents to the lender. Now, this doesn’t happen in every situation but it can and it’s something you need to be aware of.

If you are considering paying discount points or if the lender who is providing you with a quote is charging you points, you need to ask two questions.

1.How long do you plan to stay in the home?

Paying points usually only makes sense if you plan to stay in the home for a while. Probably somewhere between 10 years or more. According toNAR, the average person stays in their home for about 13 years, which up 3 years from 2008.

2. Can I get a better deal somewhere else?

We see this every day, unfortunately. Big-name online lenders charging their clients high rates and even higher discount points to do a loan. We’ve seen $9,000 in discount points for a loan where we would have charged none for a lower rate.

The point is if you are uncomfortable about the fees you owe it to yourself to shop around.

💵 LET US COMPARE RATES FOR YOU 💵

Upfront Mortgage Insurance Fees

Whenever you purchase a home and put less than 20% down you will have what’s called mortgage insurance or “PMI”. This is a monthly insurance built into your mortgage payment that you pay every month.

However, if you are borrowing using a government loan, which is about 30% of buyers, you will also have an upfront insurance fee that is financed into the loan.

The cost of the premium for FHA, USDA, and VA:

- FHA is 1.75% of the loan amount

- USDA is 1% of the loan amount

- VA is 1.25% to 3.3% but can be waived with a service-connected disability

Title Fees

The title company is another third party to the transaction and they also have fees. It’s important to note that you as the buyer have the right to chose your title company. Your lender or real estate agent may make a recommendation based on people they have used in the past.

There are generally five or six different fees that are associated with the title company:

- Title Examination ($200)

- Lender’s Endorsement Fee $(400)

- Lender’s Title Insurance ($500-$1500 varies*)

- Title Search Fee ($200)

- Settlement Fee ($375)

- Owner’s Title Insurance ($200-$1000 varies*)

On average we see title fees ranging from $1500-$2000 for our clients here in Louisiana.

Prepaids & Escrows

The prepaid and escrow portion of mortgage closing costs are the most affected by each home. These fees include home insurance, flood insurance, property taxes, and HOA dues.

Your taxes and insurance are 100% determined by the exact home you choose. We typically estimate 1% of the loan amount for property taxes and insurance as a general rule. This can vary as we will discuss below.

Property Taxes

Your property taxes are the amount of taxes each year that you will owe to the parish or county. Most tax assessors will have an online website where you can see the milage rates and use your pre-approved amount as an estimate.

The amount of taxes collected upfront as part of your closing costs varies but it’s usually 3-6 months of the annual tax amount.

Guide to Louisiana Property Taxes

Property Insurance

As we were discussing above insurance rates are a lot like mortgage interest rates. These premiums vary based on several factors such as:

- Your credit score

- Age of the home

- Claim History

- Location

- Age of Roof

- Age of HVAC and Plumbing

- The overall condition of the home

Older homes, those located near the coast, or in known natural disaster areas will often come with a higher cost.

Flood Insurance

Flood insurance is often backed by the federal government. The National Flood Insurance Program by FEMA provides insurance to help reduce the socio-economic impact of floods. This program ensures that most homes located in a flood zone can receive coverage.

Location and Elevation or the two biggest factors in flood insurance premiums. The lower a home sits to the base flood elevation, the higher the premium will be.

The location also determines the flood zone. Contrary to popular opinion, ALL homes are located in a flood zone, but not all homes require flood insurance from the lender.

We’ve seen flood insurance range from $300 per year to $10,000. Typically the only way to get a true number is to get an elevation certificate and have a local agent quote it.

Understanding Mortgage Closing Cost Estimates

When you are working with a lender to get pre-approved and to purchase a home, you will be provided with three different documents.

The Fee Worksheet

The first document you are likely to see from your lender is a fee worksheet. This is a document the lender will share with you while you are still shopping for a home.

The fee worksheet will provide you with an estimated interest rate, mortgage payment, down payment and closing costs. This is to give you a rough idea of what your costs will be.

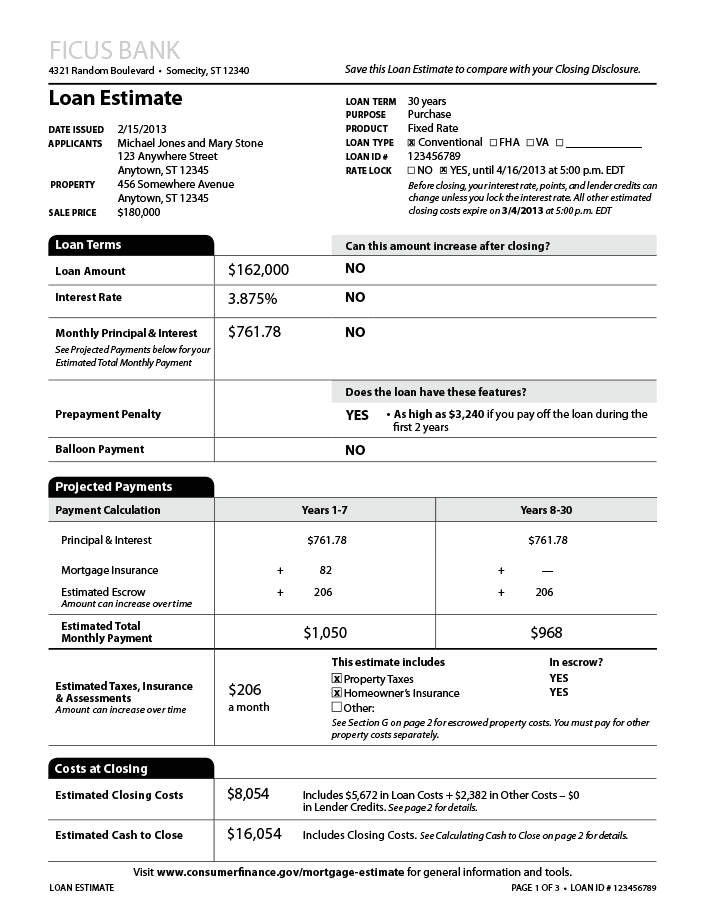

Once you find a property your lender should provide you with another document called the Loan Estimate.

The Loan Estimate

This document has all the same fees as the fee worksheet and should follow a similar format but it’s an official document. Your lender must provide this to you within 3 days of you going under contract on a home.

In addition to what’s listed in the fee worksheet, you will see if your interest rate is locked or not.

It’s important to remember that this document is an estimate, but the lender should work very hard to make sure the final numbers come in close to what’s listed here.

This document has all the same fees as the fee worksheet and should follow a similar format but it’s an official document. Your lender must provide this to you within 3 days of you going under contract on a home.

In addition to what’s listed in the fee worksheet, you will see if your interest rate is locked or not.

It’s important to remember that this document is an estimate, but the lender should work very hard to make sure the final numbers come in close to what’s listed here.

The Closing Disclosure

Finally, three days before you close your lender will provide you with a document called the Closing Disclosure. The format is very similar to your loan estimate but will be more in-depth on fees, taxes, and other items.

As you can probably tell, there are a lot of fees involved with buying a home. Preparing yourself for these costs will help you to set the right expectations and prepare your budget.

Also if looking at all of this has made you feel overwhelmed you are not alone. This is where we can really shine.

When you work with Bayou Mortgage we can help you put the plan together you need in order to own the perfect home.