You probably know that you need a good credit score to get a mortgage. But what makes a good credit score? What does a credit score include? Knowing these answers can help you maximize your score and increase your chances of securing the lowest interest rates and the best mortgage terms

What Is A Credit Scores?

Simply put, a credit score is a mathematical calculation that demonstrates your creditworthiness.

Lenders use this number as a guide to determine your loan eligibility. A higher credit score tells lenders that you are a low risk of default and a low credit score demonstrates a higher risk of default.

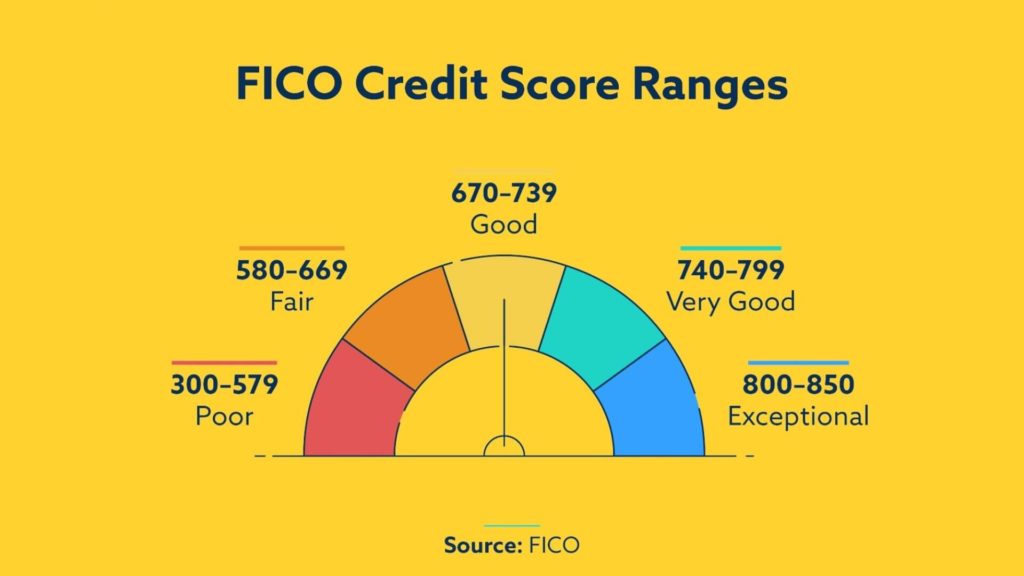

Credit scores start at 300 and go up to 850. While few people actually have an 850 credit score, many do have high scores thanks to their ability to pay their bills on time and keep their debts to a minimum.

Credit scores typically fall into a ‘range’ that gives lenders a good idea of their creditworthiness:

- 800 – 850 – Excellent

- 740 – 799 – Very good

- 670 – 739 – Good

- 580 – 669 – Fair

- 300 – 579 – Poor

Lenders use this range to choose the appropriate loan program for you.

What’s a Credit Report?

A credit report includes the history that makes up your credit score. If you order your credit report from AnnualCreditReport.com, you don’t get your credit score, but you do get a credit report from each of the three bureaus:

- Experian

- Trans Union

- Equifax

You can order one report from each bureau per year free of charge. It’s up to you how you want to order them. Order them all at once or spread them out throughout the year so that you check your credit report at least three times a year.

The credit report includes the following information

- The types of credit you have, such as revolving, installment, or mortgage

- The age of each credit account, or how long it’s been open

- The timeliness of your payments – do you pay your bills more than 30 days late?

- Your personal identifying information including your name, address, and birth date

- Information about your current and past addresses

- Information about your current and past employers

- Any public information including arrests, bankruptcies, or foreclosures

What Makes Up a Credit Score?

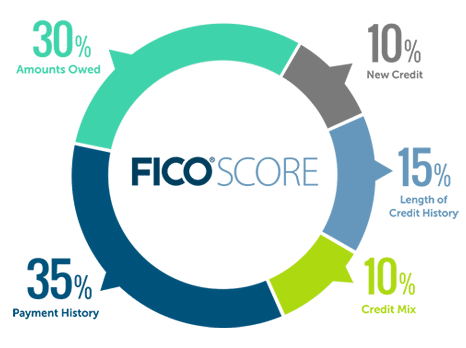

Your credit score is a number created from a complicated algorithm, but the gist of the breakdown is as follows:

- Payment history – This has the largest effect on your credit score. Pay your bills on time and you increase your chances of a high credit score. Credit bureaus only track late payments in 30-day increments. If you pay a bill late, but less than 30 days late, it won’t affect your credit score. If you pay your bills 30, 60, or 90-days late, though, it will decrease your score accordingly.

- Utilization rate – The amount of outstanding debt you have at one time affects your score quite a bit too. This is a comparison of your outstanding debt to the total available credit. For example, if you have a $1,000 credit limit and have $900 outstanding, you have a 90% utilization rate. If you have more than one credit card, your utilization rate is the total outstanding debt compared to the total of your credit lines. Ideally, you want a credit utilization rate of 30% or lower for the best credit score.

- Credit history length – Your credit history length mildly affects your credit score. It’s best to have a long credit history. You can achieve this by not closing old accounts. It’s a myth that you must use every account to keep up your credit score. Low utilization rates and on-time payments are what help your credit score. You may need to occasionally use an old card, even just for a small purchase to keep it active, though.

- Credit mix – Ideally, you want a mix of revolving debt (credit cards) and installment debt (car loans, student loans). This is only a small percentage of your credit score, though, so don’t think you need to take out a loan just to increase your credit score.

- New credit – Applying for new credit does ding your credit score slightly. But, if you want to shop around for the best rate, don’t worry about a tanking credit score. Just apply for the same loan amount within a short period. The credit bureaus recognize rate shopping and only hit you for one inquiry rather than multiple inquiries. If you apply for different types of credit during a short period, though, it can bring your score down slightly.

How Can you Raise Your Credit Score?

You need a decent credit score to get a mortgage in Louisiana. But how do you get that necessary score? Here are some easy tips:

- Make sure all payments are current – If you fell behind, get caught up as soon as you can. Get in touch with your creditors and work out a plan. Try to keep the bills out of collections as they can haunt you for years.

- Apply for a secured credit card – If you really ruined your credit and have nothing to work with, apply for a secured credit card. Your credit line will be equal to the amount you put down on the card. There’s no risk of default because the creditor keeps your deposit if you don’t make your payments.

- Apply for unsecured credit – Once you establish yourself again, apply for unsecured credit slowly. You need credit lines to build your credit score. Once you have the credit lines, pay the bills on time and don’t overextend the outstanding amount at any given time.

- Increase your credit limit – If you have a good history with specific credit card companies, consider asking for a credit limit increase. This isn’t so that you can spend more money. Instead, it’s to help lower your credit utilization rate, which helps increase your credit score.

- Keep old accounts open – Let unused credit card accounts remain open. The older your credit history gets, the more it helps your credit score.

- Pay your debts – Don’t think that you have to keep an outstanding balance on your debts. Pay off as much as you can, when you can. Showing financial responsibility in that manner helps your credit score the most.

- Use your credit regularly – Unused credit can hurt you. If you paid off all of your debt, shake things up occasionally by using your credit cards. This shows lenders your level of financial responsibility. You show that you can spend money and pay your debts back in a timely manner.

- Check your credit report for errors – Using your free access to your credit reports, check for accuracy. Human errors happen as does fraud. Check each credit line. Does it belong to you? Is the credit history accurate? If not, contact the credit bureau and creditor immediately to fix it.

How do Credit Scores Affect Your Mortgage Eligibility?

Mortgage lenders pull your credit score from Equifax, TransUnion, and Experian. They compare the scores and use the middle score for qualifying purposes. Let’s say you have the following scores:

- Equifax – 675

- TransUnion – 665

- Experian – 680

Lenders would use the 675 Equifax score to qualify you for a loan program.

Now, if you apply for a loan with a co-borrower, lenders use the lower middle score between the two borrowers. Let’s say you have the following:

You:

- Equifax – 675

- TransUnion – 665

- Experian – 680

Co-Borrower:

- Equifax – 670

- TransUnion – 668

- Experian – 685

Your middle score is 675 and your co-borrower’s middle score is 670. Lenders will use the 670 score to qualify you for the loan.

If you apply for a loan with a co-borrower, know his or her credit history so that you can decide if putting him/her on the loan is a good idea.

Your credit score determines the loan program you qualify for, such as FHA, VA,USDA, or Conventional. It also affects the amount of the required down payment and the mortgage term. It’s one of the most important factors in your mortgage eligibility.

Howdo Credit Scores Affect Your Mortgage Interest Rate?

Credit scores affect more than your ability to secure a loan. They also affect your mortgage interest rate. Lenders base your rates on your risk; it’s called risk-based pricing. A low credit score, for example, is a risk. The more risks you have, the higher the interest rate a lender charges.

Can I Buy A Home With Bad Credit?

What Else do Credit Scores Affect With a Mortgage?

Besides the eligibility and interest rates, your credit score may affect the following:

- Amount of the required down payment

- Private Mortgage Insurance rate

- Underwriting flexibility

Bottom Line

Working on your credit scores long before you apply for a mortgage in Louisiana can only work to your advantage. The higher your credit score, the more likely you are to get not only the loan approval you want, but also the attractive terms you desire. If you have any questions or concerns about your credit scores and how they affect your mortgage eligibility, let us guide you!