If you are currently going through the mortgage process you may have heard of aus. AUS stands for Automated Underwriting System. The aus in mortgage is needed in order to determine if you are able to be approved for a home loan.

AUS stands for Automated Underwriting System, and it’s a program used by mortgage lenders to determine if you can be approved for a mortgage.

The AUS is a complex computer program that runs your mortgage application and other factors through a series of algorithms that are constantly changing, to determine if your application meets the criteria set forth to receive a mortgage loan approval. There are three different types of systems that each have their own AUS findings.

What is AUS (Automated Underwriting System)?

FannieMae (FNMA)

Fannie Mae stands for the Federal National Mortgage Association, and its purpose is to purchase mortgages on the secondary market. Their work is important because they allow lenders to sell off mortgages, so they don’t have to keep those loans on their books for 30 years.

Without the secondary mortgage market, you would have a lot fewer mortgage lenders, and getting a mortgage would be much harder.

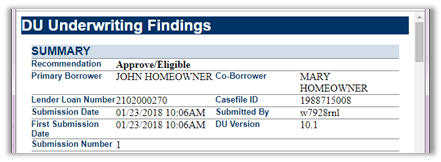

FNMA sets forth specific guidelines that mortgage lenders must follow in order to sell their loans to them. FannieMae’s AUS system called Desktop Underwriter (DU) or (DO) is designed to make sure that loans meet those requirements.

FreddieMac

FreddieMac or FHLMC is the Federal Home Loan Mortgage Corporation and just like FannieMae, they also are part of the secondary mortgage market, buying and selling home loans from mortgage lenders across the country.

FreddieMac’s AU system known as Loan Prospector (LP), is designed to make sure that the loans being sold to them meet their specific criteria.

If you are getting an FHA Loan, Conventional Loan or a VA Loan, your lender will be running your application through one or both of these automated underwriting systems.

USDA Rural Development Loans

The USDA Rural Development Loan is a program designed by the United States Department of Agriculture. It offers 100% financing for homebuyers in rural areas. However, 97% of the United States qualifies for this program so for many you may only need to go about 10 minutes outside of the city to qualify.

The USDA uses a system called GUS or Guaranteed Underwriting System.

The Guaranteed underwriting system is an AUS or automated underwriting system that lets loan officers know if your application can be approved for a Rural Development Loan.

There are 3 potential findings or results when running AUS or GUS:

- Approve/Eligible: These types of findings mean that your application has met the criteria needed to qualify for the mortgage program you are applying for. When you receive approve eligible findings it means that as long as you can prove and document your income, assets, and credit as stated on the loan application, your loan can be approved.

- Refer /Eligible: This means that your application has not met the conditions needed in order to receive an automated approval. Often the findings will tell the lender why the application isn’t receiving automated approval. These types of findings will allow you to do a manual underwrite.

- Refer with Caution: These findings mean that your application cannot be approved. Not only is your application not receiving an automated approval but it’s also not allowing the lender to do a manual approval either. Refer with caution would be a hard stop on your application.

Are AUS Findings Final?

AUS findings are only as good as the information they are given. Automated underwriting systems are reviewing your credit, income, monthly debts, down payment, reserves, and many other factors to determine if you qualify for a home.

Related: What Documents Are Needed to Purchase a Home

A good loan officer knows how to tweak your application in order to get approval. Sometimes it’s lowering your debt-to-income ratio, or grabbing your 401k statement so you can document more reserves.

Is an Automated Underwriting System Approval A Mortgage Approval?

The AUS is not a mortgage approval. Mortgage loan applications must still go through a rigorous underwriting process in order to be approved. The AUS sets the criteria for what it will take in order to receive that approval.

With an Automated loan approval through AUS your loan can only be denied if you can’t meet the criteria for the program.

The AUS makes it easier to get a home loan because your credit, income, and other factors are less likely to be as scrutinized by the underwriter. If you meet the criteria for the loan program you’ve applied for your loan will be approved.

What Should I Do if I have an AUS Refer/Eligible?

If you receive Refer/Eligible findings from the AUS, you’ll need to see if you can adjust things on your application to get an automated approval. If you can’t lower your debt-to-income ratio, increase your down payment, or provide more reserves, then you’ll need to consider manual underwriting.

What is Manual Underwriting?

Manual underwriting is the process in which your loan does not receive automated approval through AUS. When you go through manual underwriting you will have to meet more strict criteria and the underwriter will ask for more documentation.

Two of the most important things you’ll need for manual underwriting are:

Rent Verification

You need to provide the underwriter with 12 months of on-time rent payments to document that you are paying your rent on time. If you live with a family member, some lender will allow you to simply have them sign a note saying you’ve been living with them rent-free.

One to Three Months of Reserves

Reserves are money that you have left in the bank after you’ve paid your down payment and closing costs. You cannot use a gift in order to document reserves it must be your own funds, but you can use accounts like retirement or investment accounts.

The lenders are not going to take this money from you, they simply want to see that you have some cushion left over after closing the loan to prevent you from defaulting on the loan if you have hard times.

Lender Overlays and AUS

Many lenders have something called overlays that may prevent you from qualifying for a home loan. Overlays are requirements that individual lenders place on their loan programs that go above and beyond what is required by the AUS.

Examples of Overlays Include:

- Lower DTI Ratios

- High Minimum Score Requirements

- No Manual Underwriting

- More Reservers

If you were working with a lender and were denied it could be because of overlays. It’s always important when shopping for a mortgage, to work with lenders who have no overlays.

If you work with a mortgage broker that has access to multiple lenders, they will usually have lenders who will do loans based solely on the guidelines (no overlays)

Automated Underwriting System vs. Manual Underwriting

The automated underwriting system is designed to make it easier for the lender and the borrower to close a mortgage. The AUS system provides a streamlined process with less documentation which can make the process feel smoother.

However, if you are working with an experienced loan officer who isn’t afraid of a little hard work, you can get approved with a manual underwrite as well.

With a manual underwrite, you’ll need to

- have a lower debt-to-income ratio,

- have more reserves in the bank,

- be ready to explain any bad credit or late payments on your credit report.

You’ll also be required to document your rent payments with 12 to 24 months of canceled checks.

The automated underwriting system is just one way to get approval to buy a home. You don’t have to have an automated approval, you just need to be ready to fight, and work with a loan officer who knows what they are doing.